The United Kingdom’s Overseas Workday Relief (OWR) regime has undergone one of the most significant transformations in modern employment tax policy. While the primary reforms took effect from 6 April 2025, alongside the abolition of the remittance basis, the changes coming into force from 6 April 2026 represent the next phase:

consolidation, tightening of administration, and a clearer alignment between policy intent and practical delivery.

For globally mobile employees, employers, and advisers, understanding these developments is essential. The OWR regime remains a powerful relief, but it is now more structured, more transparent, and more constrained than ever before.

1. The Purpose of Overseas Workday Relief

At its core, OWR is designed to ensure that UK tax applies only to employment duties performed within the UK. Where an individual works partly overseas, the proportion of earnings relating to non-UK duties can be excluded from UK taxation, subject to specific rules.

This principle has been retained. However, the mechanism through which it operates has fundamentally changed.

2. The Post-2025 Framework: A New Foundation

From 6 April 2025, OWR was embedded within the broader Foreign Income and Gains (FIG) regime, replacing the long-standing remittance basis system. The new structure introduced several key features:

- Relief is now residence-based rather than domicile-based

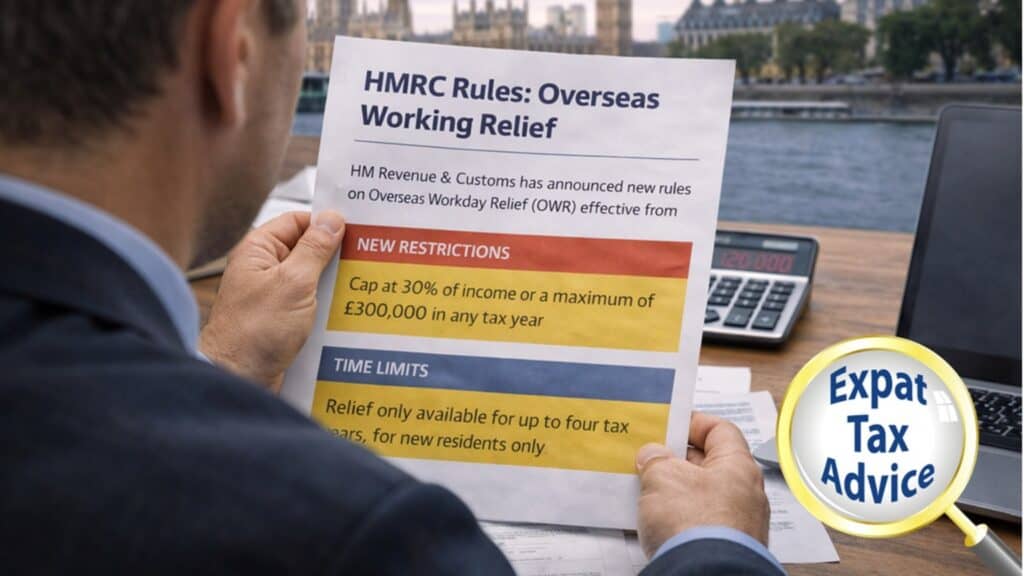

- Eligibility depends on being a “qualifying new resident” (typically after 10 years of non-residence)

- The relief applies for up to four tax years, rather than three

- There is no requirement to keep income offshore to benefit from the relief

This represented a major liberalisation in some respects, particularly the removal of the offshore restriction, which previously imposed significant administrative complexity.

However, these benefits were accompanied by new limitations.

3. The Introduction of Financial Caps

One of the most consequential changes introduced from April 2025, and central to the 2026 framework, is the imposition of a financial ceiling on relief. OWR is now limited to the lower of:

- 30% of total employment income, or

- £300,000 per tax year

This cap represents a clear policy shift. While OWR was previously uncapped (subject to remittance conditions), it is now explicitly constrained, particularly affecting high earners with substantial international duties.

4. The 2026 Reform: Aligning PAYE with Reality

From 6 April 2026, the government has taken a further step by aligning PAYE (Pay As You Earn) withholding with the capped OWR framework.

4.1 The 30% Payroll Cap

Employers will only be able to apply OWR through payroll up to 30% of an employee’s income, mirroring the statutory cap. Previously, PAYE estimates could exceed the final relief claimed, creating discrepancies between:

- Tax deducted during the year

- Final liability calculated via self-assessment

This often led to over-relief during the year, followed by corrections later.

4.2 Policy Objective

The reform aims to:

- Prevent over-claims of relief through payroll systems

- Ensure closer alignment between provisional and final tax outcomes

- Reduce administrative adjustments post year-end

In essence, the 2026 change transforms OWR from a flexible, estimation-based system into a more disciplined and predictable regime.

5. Practical Implications for Employees

5.1 Reduced Cash Flow Advantage

Under earlier systems, employees could benefit from reduced PAYE deductions based on optimistic projections of overseas workdays. The new rules restrict this flexibility, the result is:

- Less immediate tax relief through payroll

- Greater reliance on self-assessment reconciliation

5.2 Increased Accuracy Requirements

Employees must now:

- Maintain precise records of overseas workdays

- Ensure estimates used for payroll are realistic and compliant with the cap

The days of broad approximations are effectively over.

6. Implications for Employers and Global Mobility Teams

6.1 Operational Complexity

Employers must adapt payroll systems to:

- Apply the 30% cap consistently

- Align PAYE treatment with statutory limits

- Manage annual notification processes with HMRC

This increases compliance demands, particularly for organisations with internationally mobile workforces.

6.2 Risk Management

Incorrect application of OWR through payroll may result in:

- Under-withholding of tax

- Employer compliance exposure

- Reputational risk

The 2026 changes therefore place greater responsibility on employers to ensure accuracy and governance.

7. Strategic Implications for International Talent

The combined 2025–2026 reforms reflect a broader shift in UK tax policy.

7.1 From Flexibility to Structure

Historically, OWR was:

- Highly flexible

- Dependent on offshore structuring

- Generous for high earners

The new regime is:

- More transparent

- More accessible (no offshore requirement)

- More constrained (through caps and PAYE alignment)

7.2 A New Balance

The UK is seeking to balance:

- Attractiveness to global talent

- Fairness and fiscal control

- Administrative simplicity

The extension to four years and removal of offshore restrictions support competitiveness, while caps and PAYE alignment protect the tax base.

8. Interaction with the “10-Year Rule”

OWR is now closely tied to the FIG regime’s eligibility criteria. To qualify, individuals must generally have been non-UK resident for at least 10 consecutive years prior to arrival.

This has several implications:

- Returning UK nationals may benefit if they meet the threshold

- Short-term expatriates may not qualify

- The regime is clearly targeted at genuinely new arrivals, not frequent movers

9. Long-Term Outlook

The trajectory of OWR reform suggests a clear direction of travel.

9.1 Increased Standardisation

The alignment of PAYE with statutory limits indicates a move toward:

- Greater predictability

- Reduced reliance on post-year adjustments

9.2 Continued Scrutiny of High Earners

The 30%/£300,000 cap ensures that:

- Relief remains meaningful

- But not unlimited

This reflects broader international trends in taxing mobile, high-income individuals.

9.3 Integration with a Residence-Based System

The shift away from domicile and toward residence signals a more modern tax framework, aligned with global norms.

Conclusion

The changes to Overseas Workday Relief culminating in April 2026 are not incremental, they represent the final stage of a comprehensive redesign. OWR remains a valuable relief for internationally mobile employees, offering tax efficiency on overseas duties and improved accessibility through the removal of offshore requirements.

However, it is now firmly bounded by:

- Strict eligibility criteria

- Financial caps

- PAYE alignment rules

For employees, this means greater certainty but reduced flexibility. For employers, it introduces additional compliance obligations. For policymakers, it reflects a deliberate recalibration of the UK’s approach to taxing global work patterns. In a world where mobility is the norm, the UK has not withdrawn relief, but it has redefined it.

For globally mobile talent, precision, planning, and early engagement have never mattered more – contact us at info@expat-tax-advice.co.uk for active support.