If you live abroad and own, or are thinking about buying property in the UK, your tax position matters more than you think.

Because even if you don’t live in the UK…

And without the right advice, it’s easy to overpay tax, miss deadlines, or face penalties.

Yes — in most cases, you do.

If you’re a non-resident landlord, you’ll usually pay UK tax on:

You may be asking:

These are the questions that need answering before you invest — not after.

If you earn rental income from UK property while living abroad, you are still subject to UK income tax.

This means:

Without proper planning, you could:

Even as a non-resident, you will still need to pay Capital Gains Tax (CGT) when you sell UK property.

You’ll need to consider:

In many cases, you must report and pay CGT within 60 days of completion

Miss this, and penalties can apply quickly.

UK property is generally within the scope of UK Inheritance Tax, even if you live overseas. This means that your estate may still be liable to UK tax on your death, regardless of your country of residence.

In many cases, this can result in:

For non-UK residents, exposure to UK Inheritance Tax is often overlooked, particularly where property has been held for long-term investment or as part of an overseas portfolio.

With appropriate planning and structuring, it may be possible to reduce or manage this exposure and ensure that your estate is passed on in a more tax-efficient way.

With the right structure, you may be able to reduce this exposure.

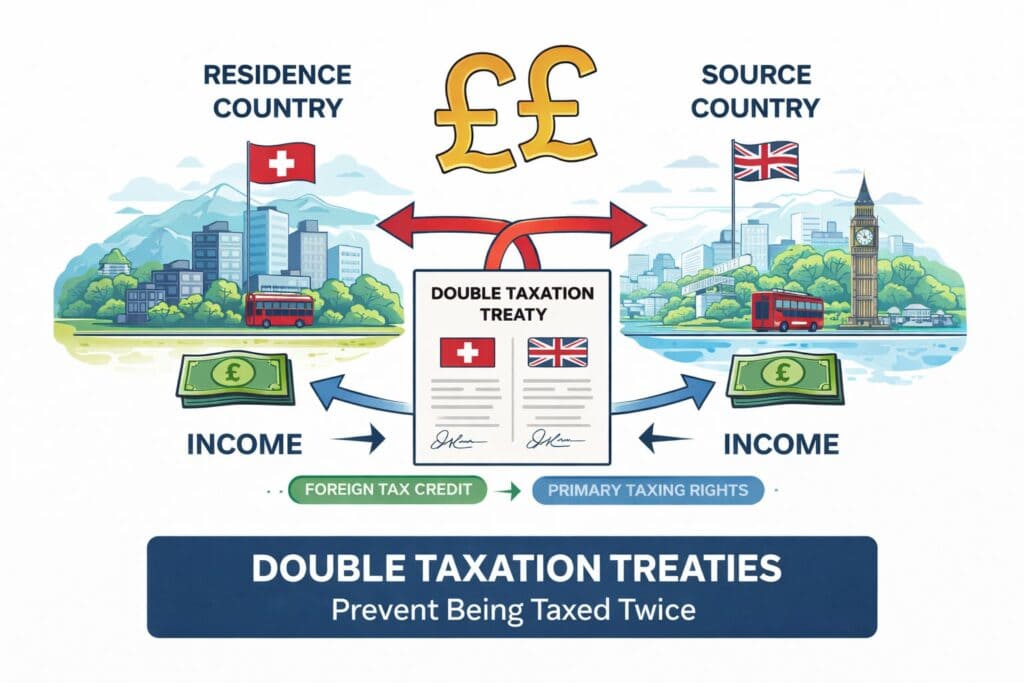

Could You Be Taxed Twice?

If you live overseas, your UK tax obligations don’t exist in isolation. Your country of residence may also tax your worldwide income and gains, which can include:

This creates a genuine risk of double taxation, where the same income or gain is taxed in both the UK and your country of residence.

However, double taxation does not necessarily mean paying tax twice. With the right advice and planning, it is often possible to:

Proper coordination between jurisdictions is key to ensuring you are not paying more tax than necessary.

How you own your UK property can make a significant difference.

You need to consider:

Get this wrong and your investment becomes tax-heavy.

Get it right and your property works for you — not against you.

You don’t need to navigate UK property tax alone.

With the right advice, you can:

This is not general advice.

This is specialist UK property tax advice for non-residents and expats.

Most problems we see come down to timing and lack of planning.

A short conversation before you buy, sell, or restructure your property can save you:

Whether you already own UK property or you’re planning your first investment, getting your tax right from the start puts you in control.

Speak to a UK expat tax specialist today

A non-UK tax resident who receives rental income from UK property must register with HM Revenue & Customs under the Non-Resident Landlord Scheme (NRLS).

As well as the experts in our team, we have a dedicated team of property experts in our sister company, www.property-tax-advice.co.uk.

If you do not register under the Non-Resident Landlord Scheme (NRLS), your agent, or tenant, if you do not have an agent, will be required to pay 20% of your gross rental income to HMRC, so make sure you tell us to register you for the scheme.

If you have registered under NRLS, then you will still be required to file a Self-Assessment return each year, but it will mean that your taxes would be calculated on the profit rather than suffering a deduction from the gross rental income at source…and if you are a UK national, from the EEA, or from countries with a double taxation agreement with the UK that grants the allowance, you’ll also get the personal allowance (2026 – first £12,570 per annum) tax free.

We will handle the NRLS registration, and the ongoing compliance as well as advising you on all matters related to your UK property including introducing you to appropriate brokers for finance etc

A non-UK resident selling a UK investment property must pay UK Capital Gains Tax (CGT) on the gain and report it to HM Revenue & Customs.

For a non-UK resident, the purchase date affects how the capital gain is calculated when selling UK investment property.

The earlier the property was bought, the more likely part of the gain (pre-2015) is outside UK tax for non-residents.

The capital gain is calculated as:

Sale proceeds – allowable costs = taxable gain

Allowable costs include:

You then:

Deduct any available Annual Exempt Amount (if eligible)

Apply the relevant CGT rate to the remaining gain

Report and pay the tax to HM Revenue & Customs within 60 days of completion

It’s the increase in value (after costs and reliefs) that is taxed, and our specialist teams will handle all your tax management and compliance.

Even though non-UK residents are subject to UK Capital Gains Tax when selling property, there are a number of reliefs that can reduce the amount of tax payable.

Private Residence Relief (PRR)

If the property has been your main home at any point, you may be entitled to Private Residence Relief. This can exempt some or all of the gain from tax. You’ll generally need to show that the property genuinely was your main residence and that you met certain UK occupancy conditions during the period of ownership. In most cases, the final 9 months of ownership can still qualify for relief, even if you were not living there at that time.

Rebasing relief

One of the most valuable reliefs available to non-residents is “rebasing.” This means that, if you purchased the property pre-2015, instead of calculating your gain from the original purchase price, you can use the property’s market value at April 2015. In practice, this often significantly reduces the taxable gain, as only the increase in value since that date is taxed.

Annual Exempt Amount

Individuals are entitled to an annual tax-free allowance for capital gains. This means that a portion of the gain can be realised without any tax being due. The allowance is relatively modest, but it can still help reduce the overall liability. For the 2026-27 tax year this is £3,000.

Loss relief

If you have made losses on other UK property disposals, these can usually be offset against your gains. This ensures that you are only taxed on your net profit across all relevant disposals.

When a non-UK resident sells a UK property, there are strict reporting requirements that must be followed.

You are required to submit a Non-Resident Capital Gains Tax return to HMRC within 60 days of completion of the sale. This deadline is significantly shorter than the usual Self-Assessment reporting timelines and often catches sellers by surprise.

Importantly, this reporting obligation applies even if:

If tax is payable, it must also be paid within the same 60-day window.

Failure to meet these deadlines can result in automatic penalties and interest, so it’s essential that the position is reviewed and reported promptly following completion.

For many expats, this is one of the most overlooked aspects of selling UK property, taking early advice and planning is key to avoiding unnecessary costs and compliance issues.