Voluntary NICs abroad changed from 6 April 2026, affecting how non-residents can maintain their UK National Insurance record and protect their future State Pension entitlement. For many expats, the loss of the lower-cost Class 2 route means National Insurance planning now needs to be reviewed much more carefully.

This change is not merely administrative; it fundamentally alters the cost, accessibility, and long-term viability of maintaining a UK National Insurance record from overseas. For British citizens who are already non-residents and those who may become so, the implications are both immediate and enduring. The key question for many non-residents is whether paying voluntary NICs abroad still represents good value under the new rules.

1. How the Pre-2026 UK NIC System Worked for Non-Residents

Historically, non-resident individuals could maintain their UK NIC record through two voluntary routes:

- Class 2 contributions: a low-cost option (approximately £3.50 per week)

- Class 3 contributions: a higher-cost alternative (approximately £17.75 per week)

Class 2 contributions were particularly advantageous. They allowed qualifying individuals—typically those who had worked in the UK prior to departure—to maintain eligibility for the UK State Pension at minimal cost. This mechanism served as a bridge between domestic employment and international mobility, supporting a globally mobile workforce.

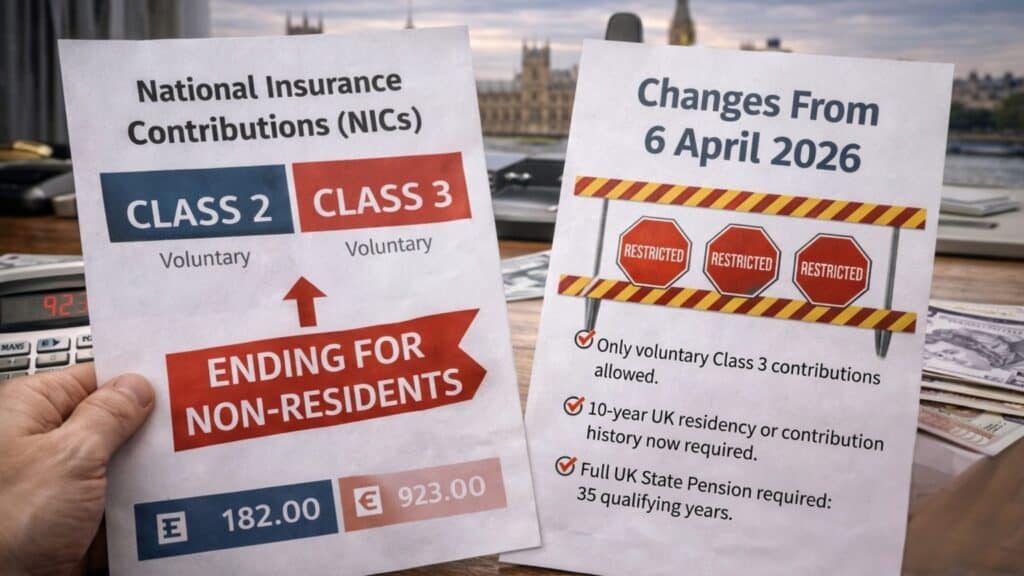

2. What changed for voluntary NICs abroad from 6 April 2026?

From 6 April 2026, this dual structure is abolished for individuals abroad.

The key legislative changes are in essence …

- Voluntary Class 2 NICs will no longer be available for periods spent abroad

- Only Class 3 contributions will be permitted going forward

This represents a deliberate withdrawal of the low-cost route for maintaining contribution records overseas. While contributions for periods before April 2026 remain unaffected, all future accrual must occur under the Class 3 regime.

3. How much do voluntary NICs abroad cost after April 2026?

The most immediate and visible consequence is cost escalation. Under current rates:

- Class 2: ~£182 per year

- Class 3: ~£923 per year

This represents an increase of approximately fivefold for each qualifying year of contributions. For individuals aiming to build or complete the 35 qualifying years

Typically required for a full UK State Pension, the cumulative cost difference is substantial. What was once a relatively modest annual expense becomes a significant long-term financial commitment.

For some expats, the higher cost of voluntary NICs abroad may still be worthwhile if it improves their eventual UK State Pension position.

4. Who can pay voluntary NICs abroad under the new 10-year test?

In parallel with increased costs, the government has introduced stricter access criteria.

From April 2026, individuals applying to make voluntary contributions from abroad must satisfy one of the following:

- Have lived in the UK for at least 10 consecutive years, or

- Have paid 10 years of NICs while in the UK

This marks a notable tightening of the regime. Previously, eligibility for Class 2 contributions required far less extensive UK ties. Under the new rules, some individuals, particularly those with shorter UK work histories, may be excluded entirely from making voluntary contributions.

5. Immediate Impact on British Citizens Already Living Abroad

For British citizens already living abroad, the short-term implications are immediate and practical:

5.1 A Closing Window for Class 2 Contributions

The 2025/26 tax year represents the final opportunity to secure qualifying years at the lower Class 2 rate. Individuals can still make backdated contributions (typically up to six years) under existing rules before the deadline.

5.2 Administrative Action Required

Those currently paying Class 2 contributions will be transitioned out of the system. HMRC has indicated it will notify affected individuals, but responsibility ultimately rests with the taxpayer to assess eligibility and decide whether to continue under Class 3.

5.3 Immediate Cost Decisions

Non-residents must now evaluate whether maintaining their NIC record remains economically viable. For some, the increased cost may outweigh the perceived benefit of additional State Pension entitlement.

6. Medium-Term Impact of the 2026 NIC Reforms on Expats

Over the medium term, the reform is likely to influence behaviour in several ways:

6.1 Will Fewer Non-Residents Pay Voluntary NICs?

The significant cost increase may discourage participation, particularly among younger expatriates or those with partial contribution histories.

6.2 Why Pre-Departure NIC Planning Matters More from 2026

Individuals planning to leave the UK may seek to maximise contributions before departure or ensure they meet eligibility thresholds. The reform introduces a new dimension to financial planning around emigration.

6.3 How the Changes Could Affect International Employers and Global Mobility

Multinational employers may face increased pressure to support employees’ pension continuity, potentially incorporating NIC contributions into expatriate compensation packages, albeit at higher cost.

7. How voluntary NICs abroad affect UK State Pension entitlement

The combined 2025–2026 reforms reflect a broader shift in UK tax policy.

7.1 Risk of Missing Qualifying Years for the UK State Pension

Individuals unable or unwilling to pay Class 3 contributions may accumulate insufficient qualifying years. This could result in reduced or even zero entitlement to the UK State Pension, particularly for those who do not meet the minimum threshold of 10 qualifying years.

7.2 How the Reforms Could Create Greater Pension Inequality Among Expats

The reforms may disproportionately affect:

- Lower-income individuals unable to afford Class 3 contributions

- Those with shorter UK work histories

- Younger professionals with fragmented careers

In contrast, higher earners may continue contributions without difficulty, widening disparities in retirement outcomes.

7.3 A Shift Toward Territoriality

From a policy perspective, the reform signals a move toward a more territorially focused system. The removal of subsidised overseas contributions reflects a view that state pension benefits should be more closely linked to domestic economic participation.

8. Strategic Considerations for Future Non-Residents

For individuals who may become non-resident after 2026, the landscape is fundamentally different:

- Early career planning becomes critical: Ensuring sufficient UK contribution years before departure may reduce reliance on expensive voluntary contributions later.

- Cost-benefit analysis is essential: The decision to pay Class 3 contributions should be assessed against expected pension benefits and alternative retirement savings options.

- Eligibility must be monitored: Failing to meet the 10-year requirement could eliminate the ability to contribute entirely.

Conclusion: Why the 6 April 2026 NIC Reforms Matter for Non-Residents

The changes to UK National Insurance rules from 6 April 2026 represent a decisive shift in how the system treats non-residents. By eliminating voluntary Class 2 contributions and restricting access to Class 3, the government has increased both the cost and complexity of maintaining a UK NIC record from abroad.

In the short term, the reform creates urgency: individuals must act before April 2026 to secure lower-cost contributions where possible. In the long term, it reshapes the economics of pension planning for expatriates, introducing higher costs, stricter eligibility, and greater uncertainty.

Ultimately, the message is clear. In an era of global mobility, the UK is redefining the balance between flexibility and fiscal responsibility. For British citizens abroad, maintaining a connection to the UK State Pension system will no longer be a low-cost default….it will be a deliberate and potentially expensive choice.

Talk to us by emailing info@expat-tax-advice.co.uk if you’re affected by this change, and perhaps it’s also time to be introduced to the international IFA’s we work with and make sure your personal pensions are properly set up.

FAQs about voluntary NICs abroad

Can non-residents still pay voluntary Class 2 NICs after 6 April 2026?

No. From 6 April 2026, voluntary Class 2 National Insurance contributions will no longer be available for periods spent abroad. Non-residents looking to maintain their UK National Insurance record will generally need to consider Class 3 contributions instead.

What is the difference between Class 2 and Class 3 voluntary NICs?

The main difference is cost. Class 2 has historically been the much cheaper option for qualifying individuals living abroad, while Class 3 is significantly more expensive. This matters because the removal of Class 2 increases the cost of protecting your UK State Pension record.

Who can pay voluntary NICs from abroad after April 2026?

From April 2026, stricter eligibility rules will apply. Individuals will generally need to have either lived in the UK for at least 10 consecutive years or paid 10 years of UK National Insurance contributions in order to qualify to pay voluntary contributions from abroad.

How do these NIC changes affect UK State Pension entitlement?

Your UK State Pension entitlement depends on how many qualifying years of National Insurance you have built up. If you cannot afford to continue contributing, or no longer meet the eligibility rules, you may end up with gaps in your record that reduce your eventual State Pension.

Should I make voluntary NIC contributions before 6 April 2026?

For some people, yes. The 2025/26 tax year may be the final chance to secure qualifying years at the lower Class 2 rate, depending on your circumstances. This is likely to be particularly relevant for non-residents who want to strengthen their UK State Pension position before the rules change.

Are backdated voluntary NIC contributions still possible before the deadline?

In many cases, individuals may still be able to make backdated voluntary contributions for previous tax years, subject to HMRC rules and deadlines. This can be an important planning opportunity before the April 2026 changes take effect.

Is paying Class 3 still worth it for expats after April 2026?

That depends on your wider retirement position, expected UK State Pension entitlement, age, and whether you have other pension provision in place. For some, Class 3 will still represent good value. For others, the higher cost may mean alternative retirement planning options are more attractive.

What should British citizens living abroad do now?

They should review their National Insurance record, check whether they currently qualify for voluntary Class 2 contributions, and assess whether action should be taken before 6 April 2026. Leaving it too late could mean losing access to the lower-cost route permanently.